Risk Retention Groups in Trucking: Benefits, Regulation, and Challenges

Risk retention groups (RRGs) serve as an important liability insurance solution for motor carriers across the nation. In addition to filling a liability insurance gap in trucking, the unique structure and regulation standards of RRGs enable them to provide tailored underwriting and additional benefits for their members that result in stable, quality, and affordable coverage. Despite their positive impact in the trucking industry, risk retention groups are sometimes misunderstood. Misunderstanding of RRGs and a lack of freight fraud enforcement poses challenges for the future of RRGs. In order to ensure that all responsible motor carriers continue to have access to liability coverage, it is important for the trucking industry to better understand risk retention groups and help support them and the essential role they play.

What are Risk Retention Groups and Why Were They Created?

Risk Retention Groups were developed by Congress as a solution to address the challenges businesses, organizations, and governmental units faced in obtaining liability insurance. During the liability insurance crisis of the 1970s, escalating liability insurance premiums, strict liability, runaway verdicts and the onset of bad faith and other unfair practices laws created an environment that made liability coverage unavailable or unaffordable across numerous industries.

In response, Congress passed the Products Liability Risk Retention Act (PLRRA) in 1981, and then expanded the PLRRA’s reach to all forms of liability insurance with The Federal Liability Risk Retention Act of 1986 (LRRA). Congress designed the PLRRA and the LRRA to encourage the formation and growth of risk retention groups: an alternative insurance model that enables businesses or organizations facing similar risks to form a liability insurance company that is owned and operated by its members, enabling coverage to be tailored to address the group’s specific needs and risks. Congress recognized that member-owned insurance companies—where the insureds have direct governance and financial stake in sound underwriting—offered a viable alternative to a traditional market that had proven itself unreliable. RRGs have continued to prove their value not just as temporary options during hard markets, but as long-term solutions with a member-first approach for better risk management and coverage.

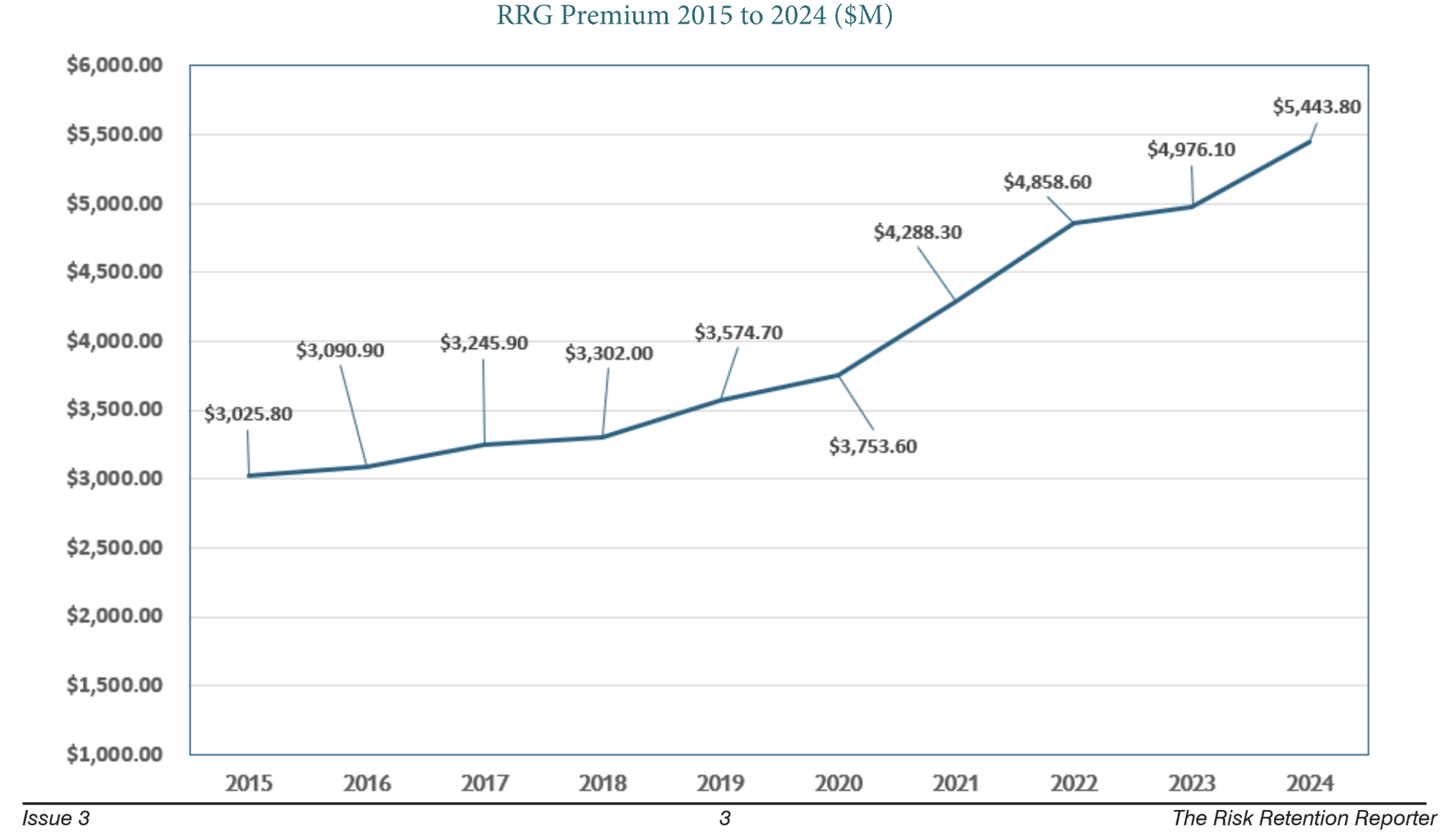

Forty years later, risk retention groups continue to serve their original purpose and fill a significant gap in liability insurance to this day. There are 239 active RRGs operating in the United States across healthcare, transportation, construction, education, and other sectors, collectively writing approximately $5.5 billion in annual premiums and providing liability coverage to many businesses in a way that is uniquely suited to cover their industry-specific risks.

In fact, according to the Risk Retention Reporter (2025, Vol. 39, Issue 3), risk retention groups have increased in gross written premium for the last 14 consecutive years, indicating they are stronger than ever.

Risk Retention Reporter. Vol. 39, no. 3, 2025. Risk Retention Reporter, LLC.

Risk Retention Groups’ Critical Role in Trucking: Filling the Liability Insurance Gap

Risk retention groups play a vital role in preserving the existence of responsible motor carriers for the U.S. trucking industry. The traditional insurance market has a repeated history of failing to provide adequate and stable liability coverage for motor carriers. The admitted market routinely exits a territory, class of business, or segment of business when claims get expensive in the face of historically underpriced policies, leaving all motor carriers without coverage, irrespective of how well they manage their risk. When this happens, risk retention groups step in to fill the void and provide liability insurance to the responsible motor carriers the admitted market will no longer cover. RRGs have served as a successful solution to provide affordable and quality liability insurance for responsible motor carriers for years, precisely as they were designed to do as created under the Liability Risk Retention Act. In fact, the need for risk retention groups in trucking has continued to grow, as evidence by increased premium of 36.8% from 2023 to 2024 alone (Risk Retention Reporter, 2025, Vol. 39, Issue 3). Without the help of risk retention groups, many responsible motor carriers nationwide would lose coverage with no alternative coverage option, forcing them to close their businesses or drive without coverage.

Benefits Beyond Coverage: Advantages of Risk Retention Groups for Motor Carriers

Risk retention groups have the ability to leverage their unique structure to provide customized services to motor carriers while also maintaining stable coverage and affordable long-term costs.

Take, for example, the Owner-Operator Independent Drivers Association (OOIDA), which has served owner-operators since the late 1980s and remains one of the most experienced commercial truck insurance specialists in the country, insuring over 26,000 motor carriers with an exemplary safety profile. Originally founded as a transportation member organization and advocacy group in 1973, OOIDA went on to form one of the first—and now the longest-operating—transportation RRGs. In addition to providing liability coverage to its motor carriers, OOIDA has developed expansive ancillary programs to meet motor carriers’ evolving needs including life and health benefits, a drug and alcohol testing consortium, a permits and licensing group, and a compliance unit. OOIDA also leverages its extensive knowledge of the trucking industry to provide trusted information sources to its motor carriers, including Land Line Magazine—the most widely circulated trucking periodical in the U.S.—and a daily SiriusXM satellite radio show.

Below is a breakdown of a few of the unique characteristics of RRGs that OOIDA and other successful trucking RRGs leverage to benefit the motor carriers they insure.

Designed to Serve Motor Carriers, Not Generate Profits

Unlike traditional insurance companies, which frequently focus on profits, risk retention groups operate for the benefit of their motor carriers and the trucking industry as a whole. Because policyholders are also owners, they directly influence governance and can achieve greater stability, flexibility, and control over their insurance programs compared to traditional insurance entities. Unlike traditional entities, which sell to the general public seeking to generate profit, risk retention groups write coverage for their group members only.

Policies and Underwriting Tailored for Carrier-Specific Risks

Operated and led by members of the trucking industry, risk retention groups’ first-hand knowledge gives them the ability to offer tailored policies and underwriting for the unique risks of their motor carriers, help members navigate shifting regulatory and market conditions in real-time, and share knowledge to stay ahead of emerging risks.

True Value-Add Services

RRGs often utilize their boots-on-the-ground awareness to offer complimentary lines or other value-add services to help address their motor carriers’ most pressing needs such as regulatory assistance, relevant training and education, and even advocacy on members’ behalf.

Proactive Risk Management and Safety

Due to the shared nature of their member-owned structure, risk retention groups assist with and enforce proactive risk management, operational best practices, and high safety standards. Every carrier in the group must actively engage in risk reduction efforts to ensure that the whole group remains financially strong. Proactive risk mitigation also helps to keep premium costs down for the group, incentivizing the participation of each member.

Quicker, More Efficient Claims Management

Risk retention groups address claims swiftly to help protect both its motor carriers and claimants, often employing early intervention strategies to identify and address root causes before they escalate, minimize liability and exposure, and reduce the overall frequency and severity of claims.

Long-Term, Stable Coverage and Affordable Prices

Unlike traditional insurers that may withdraw from a market during tough times, risk retention groups are designed to succeed over time when all of its members share a long-term commitment to risk management. The outcome is stable coverage and affordable pricing.

Risk retention groups’ carrier-first approach, tailored coverage and services, first-hand industry knowledge, and a proactive risk management and safety strategy allow RRGs to provide unmatched advantages for their motor carriers compared to traditional insurance providers. Another distinct asset of risk retention groups is their unique regulatory structure.

Regulation of Risk Retention Groups in Trucking: A Valuable Asset

The unique regulatory structure of risk retention groups allows them to operate more efficiently across states. Although risk retention groups are an alternative to traditional liability insurance, they are no less diligently regulated and scrutinized, and its domiciliary regulators are held to the same accreditation standards that apply to their regulation of traditional insurers.

Single State Licensing

Risk retention groups must be chartered (licensed) and regulated by a single state, known as the “domiciliary state.” Once chartered, an RRG can operate in all other states as a “foreign” RRG by filing the appropriate registration paperwork. Regardless of how many states an RRG operates in, it is regulated solely by its domiciliary state, and federal law limits how much other states can govern its operations. This is unlike traditional insurers, which must obtain a separate license in every state where they conduct business and must adhere to state-specific regulation requirements in each of those states. This regulatory distinction for RRGs was decided by Congress as a pathway to help RRGs to get the coverage they need across state lines.

Accountability and Oversight

Domiciliary regulation of risk retention groups is a robust process dictated by federal standards set in the LRRA and by the National Association of Insurance Commissioners (NAIC) accreditation standards. RRGs are required to submit the same key filings as traditional insurers including annual and quarterly financial statements, actuarial opinions, revisions to their plan of operation, and notices of material events (e.g., changes in management, ownership, risk profile, etc.). RRGs are subject to regular exams and audits by their domiciliary regulators. The NAIC accreditation teams also review the domiciliary regulators’ handling of risk retention groups rigorously.

Domiciliary State Requirements

As the RRG’s sole regulator and primary point of oversight, the domiciliary state ensures the group remains financially sound and in compliance with both state and federal law. The domiciliary state is also responsible for licensing authority and the day-to-day operational requirements of the RRG with a focus on solvency, governance, and operational accountability.

Domiciliary state-level requirements include:

Legal structure: An RRG must be formed as a stock, mutual, or reciprocal insurance company under state law.

Minimum capital and surplus: The domiciliary state sets financial thresholds to ensure solvency and protect policyholders.

Plan of operation approval: The RRG must submit a detailed feasibility study and plan of operation for review and approval before offering insurance.

Board governance: RRGs are overseen by a board of directors elected by member-policyholders, typically with at least one resident director from the domiciliary state.

Reinsurance Programs: RRGs obtain reinsurance to further increase an RRG’s capacity to cover claims and damages, backstopping the RRG with deep pocket reinsurers.

Required service providers: Most states require engagement of a licensed captive manager, independent CPA, and qualified actuary, vetted and approved by the state regulators to maintain financial reporting and compliance.

Operating in Foreign/Non-Domiciliary States

Before an RRG may operate in a non-domiciliary state, the RRG must register to do business in the state and provide the state with a copy of its feasibility study that was approved by the domiciliary state as well as any revisions to that study submitted to the domiciliary state. The RRG must also provide annual audited financial statements and statements of opinion on loss and loss adjustment expense by an actuary or qualified loss specialist. Although the LRRA broadly preempts most non-domiciliary state insurance laws, it does carve out anarrow set of exceptionswith which RRGs must comply when operating in other states.

Guaranty Funds, Financial Safeguards and Insolvency Risk

Insolvency is a risk for both traditional insurers and RRGs alike, and each have their own structures that address insolvency risk. Traditional insurers rely on mandated guaranty funds to help cover damages if the company becomes insolvent. However, full coverage of damages is not actually “guaranteed“ because coverage from guaranty funds can vary from $100,000 - $750,000 depending on the state. This means that if a traditional insurer becomes insolvent, the maximum amount of money the claimant will receive is between $100,000 - $750,000, even if the claim is more. In instances of multimillion and nuclear verdicts, coverage from the guaranty fund is insignificant.

For political reasons, the drafters of the LRRA excluded risk retention groups from participating in state guaranty funds. Instead, RRGs take a more proactive approach to guard against insolvency. RRGs maintain multiple layers of financial safeguards including their mandatory capital and surplus requirements set by domiciliary regulators, independent actuarial reserve analyses, regular financial examinations by state insurance departments, regulation by state domiciles and the NAIC, and member assessments that can be levied in the event of adverse development. These mechanisms provide meaningful protection for RRGs.

Almost all risk retention groups are also required to carry reinsurance by their state domicile to further multiply their ability to cover claims and handle losses.

The unique structure of RRGs further enhances safety and financial protection. To maintain the wellbeing of the entire group, RRGs can be extremely discerning about who they let join the group. Member ownership creates self-interest for RRGs and incentivizes them to operate responsibly, uphold safety best practices, investigate and vet new members, and practice risk mitigation. Skin-in-the-game governance allows RRGs to respond to the evolving risks of their motor carriers and maintain protections that address these risks accordingly to prevent claims and mitigate risks in the first place.

The single-state licensing model is ultimately a valuable asset that allows RRGs to operate across states more efficiently while maintaining accountability, rigorous oversight from domiciliary states, and the same accreditation standards that apply to traditional insurers.

Challenges for Risk Retention Groups in Trucking

A lack of freight fraud enforcement combined with misunderstanding born from misunderstanding about risk retention groups is creating significant challenges for risk retention groups in trucking.

Increased Criminal Activity in Trucking and Lack of Enforcement of Trucking Regulations

For years, the trucking industry as a whole has been experiencing an ongoing increase in freight fraud, resulting in increasingly complex claims. Types of fraudulent activities on the rise span from identity theft scams to staged accidents to cargo theft, which alone has increased over 1,200% since 2021.

One of the most significant challenges pertaining to freight fraud for RRGs is that the current federal structure of obtaining carrier insurance does not actively enforce the law or penalize criminal activity. For example, If a carrier intentionally misrepresents their operations to obtain coverage and then operates far outside of the scope that was represented - running 250 trucks on a policy written for 30, operating drivers with disqualifying records, shuffling vehicles between affiliated DOT numbers - the carrier faces no financial liability or meaningful consequences when an inevitable crash ensues. Even more alarming, the carrier will typically simply close down and reopen under a new name and DOT number. This is a dangerous cycle that threatens both public safety and the existence of risk retention groups that become victims of this type of fraud.

Misunderstanding of Risk Retention Groups

General misunderstandings about risk retention groups cause them to encounter significant misunderstanding within the trucking supply chain. Many shippers and transportation platforms exclude or restrict RRG participation due to confusion around solvency, AM Best ratings, or group-based liability coverage.

Misunderstanding of risk retention groups in trucking has been exacerbated further after the failure of Spirit Commercial Auto Risk Retention Group, Global Hawk Insurance Company Risk Retention Group, and Federal Motor Carriers Risk Retention Group - run by two individuals who engaged in criminal activity and effectively cast a shadow over the public perception of RRGs. These failures were not the result of any insufficiency with regard to the RRG model. Criminal activity and fraud can, unfortunately, take place in both traditional insurance companies and non-traditional entities like RRGs, and one model is not more susceptible than the other. Spirit, Global Hawk, and Federal Motor Carriers are outliers in RRG history, not the norm, and should not discount the hundreds of other RRGs that have operated responsibly over nearly four decades.

Paving a Way Forward in Trucking, Together

Risk retention group education along with fraud and safety reform are two necessary initiatives that the trucking industry must work together on to help ensure RRGs can continue to fill the liability insurance gap in trucking for years to come.

Risk Retention Group Education

Industry-wide education around RRGs including their strength and stability, exemplary risk mitigation practices, maintained accreditation standards and regulatory oversight, and the essential role they play in trucking is needed to prevent misunderstanding and help trucking RRGs compete on a level playing field.

As the nation’s leading network of risk retention group experts, NRRA provides industry-specific RRG training, educational resources, and events. Reach out to NRRA’s executive director to learn more about educational opportunities.

Fraud and Safety Reform

Fraud detection infrastructure (such as cross-referencing insurance filings across affiliated DOT numbers), penalties for application fraud, real-time fleet verification requirements, and personal liability for principals of motor carriers found to commit fraud are critically needed from the FMCSA to reverse increasing fraud in trucking.

NRRA welcomes members of the trucking industry to work alongside our transportation committee to advocate for reforms to improve trucking safety and protect the RRG structure and its benefits for motor carriers.

Conclusion

Risk retention groups provide an essential service for motor carriers seeking stable and affordable liability insurance, but misunderstanding of RRGs and freight fraud put this important liability insurance model at risk.

The RRG industry stands ready to work with regulators, legislators, and industry stakeholders to provide education on risk retention groups to the trucking industry and help push forward meaningful reforms that target bad actors while preserving the RRG model that many of motor carriers depend on.

About the National Risk Retention Association

The National Risk Retention Association (NRRA) is the only nonprofit organization solely dedicated to supporting risk retention groups and risk purchasing groups nationwide. Through advocacy, education, and industry collaboration, NRRA works to protect the integrity of the Liability Risk Retention Act and support the long-term success of the RRG industry.

About the Risk Retention Reporter (RRR)

The Risk Retention Reporter (RRR) is a long-standing independent industry publication focused on regulatory, legal, and market developments affecting risk retention groups and risk purchasing groups. It provides in-depth reporting and analysis used by RRG professionals, regulators, and industry stakeholders.